ChatGPT Is No Longer OpenAI’s Most Important Product: How Codex Is Reshaping the Company’s Future

ChatGPT Is No Longer OpenAI’s Most Important Product: How Codex Is Reshaping the Company’s Future

By Markos Symeonides

Published for June 2026 analysis.

Executive Thesis: OpenAI’s Center of Gravity Has Moved From Chat to Work

For most of the public, OpenAI still means ChatGPT. The chatbot remains the company’s most recognizable brand, the product that brought generative AI into mainstream culture, and the interface through which hundreds of millions of users experience large language models. But inside enterprise procurement cycles, developer teams, and investor narratives, a different product family is increasingly defining OpenAI’s future: Codex and its surrounding agent infrastructure.

The strategic shift is not that ChatGPT is declining in relevance. It is that ChatGPT is becoming the surface layer for a broader agentic platform, while Codex is becoming the monetizable engine underneath. In 2023 and 2024, the winning question for OpenAI was, “How many people will pay for a better chatbot?” In 2026, the more important question is, “How many companies will pay for AI systems that can ship software, operate tools, manage workflows, and produce measurable labor leverage?”

That distinction matters because revenue quality in enterprise AI is changing. Consumer ChatGPT subscriptions are high-volume and strategically important, but they are vulnerable to churn, feature commoditization, and price sensitivity. Enterprise agent products, by contrast, attach to software delivery, infrastructure automation, support operations, compliance workflows, internal tools, and proprietary codebases. Once embedded, they become part of how a company operates. That makes Codex not merely another OpenAI product, but a wedge into the operating fabric of modern enterprises.

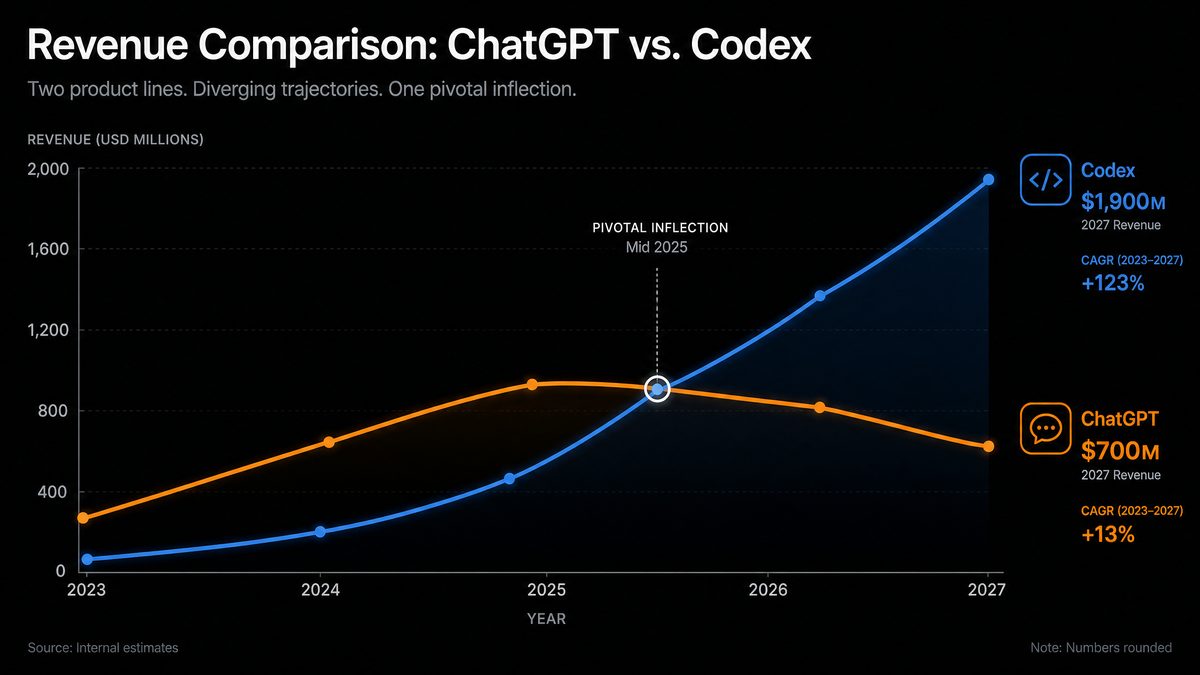

OpenAI has not published audited product-level revenue by ChatGPT consumer, ChatGPT Enterprise, Codex, and API in the manner a public company would disclose segment revenue. As a result, any precise breakdown must be treated as an informed estimate based on reported customer adoption, enterprise contract patterns, public product packaging, partner disclosures, and market intelligence from the AI infrastructure ecosystem. The directional evidence, however, is increasingly difficult to ignore: the highest-value accounts are paying not just for conversation, but for agency, tooling, and execution.

The clearest way to understand OpenAI’s transition is to separate “ChatGPT as product” from “ChatGPT as interface.” As a product, ChatGPT competes with Claude, Gemini, Perplexity, Microsoft Copilot, and an expanding set of vertical AI assistants. As an interface, ChatGPT can become the universal front door to OpenAI’s agents, including Codex-based software engineering capabilities, business process automation, data analysis agents, and task-specific enterprise assistants. That means ChatGPT may remain the face of OpenAI even as Codex becomes its most important commercial engine.

The consequences are significant. OpenAI’s IPO narrative, whenever it materializes, is unlikely to be built primarily around chatbot subscriptions. A chatbot story is a consumer growth story with platform potential. A Codex-centered story is an enterprise automation story with recurring revenue, high switching costs, developer ecosystem lock-in, and expansion across every knowledge-work function that touches software. That is a much larger and more durable market, and it explains why Codex has become central to OpenAI’s future.

The Evidence: Codex Is Becoming the Enterprise Revenue Leader

The most important evidence behind the shift is not brand recognition; it is buyer behavior. Enterprise customers are increasingly evaluating AI tools by whether they can reduce engineering backlogs, accelerate migration projects, improve security remediation, generate internal applications, and automate operational workflows. In those contexts, a general-purpose chatbot is useful, but an agent that can understand a codebase, invoke tools, write tests, open pull requests, execute commands, and maintain context across tasks is far more valuable.

Codex revenue appears to be outpacing consumer ChatGPT revenue in high-value enterprise channels because the purchasing motion is fundamentally different. A ChatGPT Plus or Pro subscription is typically an individual or team productivity purchase. A Codex deployment is often justified against engineering labor budgets, cloud transformation budgets, DevOps budgets, cybersecurity budgets, and modernization initiatives. That moves the conversation from “Is this worth $20 or $30 per user per month?” to “Can this reduce a six-month migration program, automate 40 percent of repetitive engineering tasks, or help a platform team manage 5,000 internal repositories?”

Enterprise AI buyers are also more willing to accept premium pricing when the product connects directly to measurable output. Software engineering is one of the easiest domains in which to quantify impact. A company can measure pull request throughput, test coverage, defect resolution time, migration velocity, incident response automation, developer onboarding speed, and code review cycle time. Codex gives procurement teams and CFOs a clearer productivity model than conversational AI alone.

This explains why Codex’s revenue profile can become larger than ChatGPT consumer subscriptions even if ChatGPT has more users. Consumer AI products win by scale. Enterprise agent products win by annual contract value, account expansion, and integration depth. A Fortune 500 Codex agreement can be worth more than hundreds of thousands of individual subscriptions if it is tied to engineering seats, usage-based agent runs, private codebase indexing, compliance guarantees, premium support, and custom deployment architecture.

| Revenue Stream | Typical Buyer | Pricing Logic | Expansion Driver | Strategic Importance in 2026 |

|---|---|---|---|---|

| ChatGPT Consumer | Individuals, students, creators, professionals | Monthly subscription tiers and premium model access | User growth, retention, multimodal features, personalization | Brand scale and mass-market distribution, but less enterprise lock-in |

| ChatGPT Enterprise | Large organizations and departments | Seat-based contracts, governance, admin controls, security commitments | Knowledge work adoption across functions | Important enterprise entry point, especially for non-technical workers |

| Codex | Engineering organizations, platform teams, IT, DevOps, security teams | Enterprise contracts, usage-based agent execution, repository indexing, premium integrations | Workflow automation, codebase integration, toolchain dependency, repository expansion | Core enterprise revenue driver and platform wedge |

| OpenAI API | Developers, startups, software vendors, enterprises | Token usage, model access, fine-tuning, batch processing, tools | Application growth, embedded AI features, model upgrades | Foundational infrastructure business, but more exposed to model commoditization |

The phrase “Codex is generating more enterprise revenue than ChatGPT consumer subscriptions” should be interpreted carefully. Consumer subscriptions remain enormous as a standalone business and are central to OpenAI’s distribution power. But the enterprise revenue pool around Codex is becoming more valuable because it combines software development budgets with usage-based AI economics. If Codex is deployed across a global engineering organization, its consumption can grow with every repository, build pipeline, migration project, and automated workflow.

The market signal is particularly strong among large companies that already experimented with general AI assistants. In 2024 and 2025, many organizations rolled out chat-based assistants and discovered that adoption was uneven. Employees used them for drafting, summarizing, brainstorming, and analysis, but the value was diffuse. Codex-style agents, by contrast, can be assigned to well-defined operational work. They can update dependencies, generate migration plans, refactor services, write unit tests, create documentation from code, and triage common software defects. That makes the return on investment more concrete.

The revenue dynamics driving Codex’s ascendance are clearly reflected in OpenAI’s confidential S-1 filing. Our detailed analysis of the IPO documentation reveals how Codex’s enterprise revenue now dominates OpenAI’s financial narrative, with API and agent services accounting for the majority of projected growth through 2027. OpenAI’s Path to IPO: What the S-1 Filing Means for ChatGPT, Codex, and Enterprise Customers

Another important clue is OpenAI’s product language. The company’s messaging has gradually moved from “chat with an AI” toward “delegate work to AI.” That shift is visible across agents, tool use, multimodal workflows, code execution, and enterprise integrations. Codex sits at the intersection of all of those capabilities. It is not merely a coding assistant; it is a proof point for a more general model of AI labor, where software is the first domain because the tools, artifacts, evaluation metrics, and feedback loops are already digital.

The Merger Plan: Codex Capabilities Are Moving Directly Into ChatGPT

The most consequential product strategy is not to keep Codex and ChatGPT separate forever. OpenAI’s long-term advantage comes from combining ChatGPT’s familiar interface with Codex’s action-oriented capabilities. In practical terms, that means ChatGPT evolves from a conversational assistant into an orchestration layer where users can ask for outcomes and the system routes work to specialized agents, including Codex agents that can operate across code repositories, terminals, deployment systems, documentation, and collaboration tools.

This merger strategy is commercially elegant. ChatGPT already has the distribution, brand trust, user identity system, memory layer, enterprise administration, and multimodal interface. Codex has the higher-value execution model. Integrating the two allows OpenAI to convert everyday ChatGPT usage into agentic workflows without requiring users to adopt an entirely separate product. A product manager could describe a feature in ChatGPT, a developer could authorize Codex to inspect the relevant repository, and a team lead could review the resulting pull request from the same workspace.

For enterprises, the merged experience reduces adoption friction. Companies do not want a new AI tool for every department. They want governed AI systems that connect to existing identity providers, data controls, audit logs, and compliance policies. If ChatGPT becomes the front end for Codex, then OpenAI can sell a unified enterprise platform: chat for knowledge work, Codex for engineering execution, API access for custom applications, and agent frameworks for specialized workflows.

The strategic logic resembles the way cloud platforms evolved. Early cloud adoption often began with compute or storage, but the real lock-in came from managed services, identity, monitoring, security, data tools, and developer workflows. OpenAI’s version of that platform expansion begins with ChatGPT as the accessible user experience and deepens through Codex as the operational layer. The more tasks Codex performs inside an organization, the more OpenAI becomes embedded in the company’s production workflows.

There is also a model-training advantage. With appropriate privacy boundaries, enterprise controls, and opt-in data arrangements, agentic workflows generate richer feedback than chat interactions alone. A chat response can be rated positively or negatively, but a Codex task produces structured signals: whether tests passed, whether a pull request was accepted, whether a deployment succeeded, whether a security scan flagged an issue, whether reviewers requested changes, and whether the generated code survived in production. These signals are extremely valuable for improving agent reliability.

The integration of Codex into ChatGPT also creates a new user mental model. The user no longer asks, “What should I write?” or “How do I solve this problem?” The user asks, “Can you do this?” That shift from advisory AI to execution AI is the defining product transition of 2026. In this model, ChatGPT becomes less like a search box or messaging app and more like a command center for delegated work.

Why This Matters: From Conversational AI to Agentic AI

The first wave of generative AI monetization was built around conversation. Users typed prompts, models returned text, images, code snippets, summaries, and analysis. That interface was powerful because it made AI accessible. It also had a ceiling: the user still had to move the output into real workflows. A chatbot could draft an email, but the user had to send it. It could suggest code, but the developer had to integrate it. It could propose a plan, but a human still had to execute the steps.

Agentic AI changes the value proposition by collapsing the distance between recommendation and action. An agent can use tools, observe results, adapt its plan, and continue working toward a goal. In software engineering, this means an AI system can inspect a repository, modify files, run tests, fix errors, and prepare a pull request. In business operations, it can update records, reconcile documents, generate reports, trigger workflows, and escalate exceptions. The economic value comes from completed tasks, not just useful answers.

Codex is important because software is the natural proving ground for agents. Code repositories are structured environments. Tests provide immediate feedback. Version control creates a reversible audit trail. Pull requests provide human review gates. Build systems produce objective pass-fail signals. Documentation, logs, issue trackers, and dependency graphs give agents the context they need to work. Compared with many physical or ambiguous business environments, software engineering offers a relatively measurable path to trusted autonomy.

This is why the shift from ChatGPT to Codex is not merely a product preference; it reflects the maturation of the entire AI market. Enterprises are moving beyond pilot programs that showcase impressive demos. They want AI systems that connect to workflows, produce traceable outputs, comply with governance requirements, and justify budget expansion. Conversational AI created awareness. Agentic AI creates operational leverage.

There is also a competitive reason OpenAI must make this transition. Text generation is becoming commoditized at the interface level. Multiple model providers can generate strong prose, summarize documents, answer questions, and write basic code. The durable advantage shifts to systems that combine frontier models with tools, memory, permissions, workflow design, evaluation, and data integration. Codex is OpenAI’s clearest attempt to build that durable advantage in a domain where customers will pay premium prices.

OpenAI’s strategic acquisition of Ona further demonstrates the company’s commitment to making Codex the centerpiece of its enterprise strategy. Our coverage of the Ona acquisition explains how persistent cloud environments will enable multi-day agent workflows that fundamentally change how enterprise development teams operate. OpenAI Acquires Ona: How Persistent Cloud Environments Will Transform Codex for Enterprise

The technical challenge is reliability. An agent that only chats can be wrong with limited consequence. An agent that changes production code, updates infrastructure, or modifies business systems must be constrained, observable, and auditable. That is why OpenAI’s enterprise Codex strategy depends not only on model intelligence but also on sandboxing, permissioning, test execution, policy enforcement, code review integration, secrets management, and administrative controls. The product is no longer just the model; it is the full execution environment around the model.

Revenue Breakdown: ChatGPT Consumer, ChatGPT Enterprise, Codex, and API

Because OpenAI is not a public company as of this June 2026 analysis, product-level revenue breakdowns are best understood as market estimates rather than official filings. The following table is a directional framework for understanding the changing revenue mix. It is designed to illustrate why Codex can become strategically more important than ChatGPT consumer revenue even if ChatGPT remains the larger cultural brand.

| Segment | Estimated 2026 Revenue Character | Margin and Cost Considerations | Growth Quality | Key Risk |

|---|---|---|---|---|

| ChatGPT Consumer | Large recurring subscription base with global reach and premium tiers | Inference costs remain significant; consumer pricing limits gross margin expansion | Strong brand-led growth, but dependent on retention and feature differentiation | Consumer churn, free alternatives, bundled AI from device and OS providers |

| ChatGPT Enterprise | High-value seat-based contracts for secure workplace AI | Better pricing power than consumer; support and compliance costs increase with scale | Strong if usage expands across departments and data connectors | Enterprise adoption may plateau if use cases remain advisory rather than operational |

| Codex | Fast-growing enterprise revenue tied to engineering automation and agent execution | Compute-intensive, but premium pricing and measurable ROI can support strong economics | Very strong due to workflow lock-in, repository expansion, and usage-based scaling | Reliability, security, liability, and competition from developer platforms |

| API | Broad infrastructure revenue from developers and AI-native applications | Scale benefits but exposed to model price compression | High volume, especially for embedded AI applications and vertical software vendors | Commoditization, multi-model routing, open-weight alternatives |

The consumer business remains strategically useful for several reasons. It gives OpenAI a direct relationship with users. It creates a global testing ground for new interaction patterns. It builds brand trust before enterprise adoption. It also allows OpenAI to introduce agentic features to a broad audience gradually. But from a revenue-quality perspective, consumer subscriptions are not the same as enterprise automation contracts.

ChatGPT Enterprise occupies a middle position. It is more defensible than consumer subscriptions because it includes governance, security, administrative controls, and company-wide deployment. However, if users primarily use it for writing, summarization, research, and brainstorming, its economic value can still be hard to quantify. Enterprises often begin with ChatGPT Enterprise as a safe way to introduce AI, then expand toward Codex when they want measurable operational impact.

Codex is different because it maps directly to one of the largest cost centers in modern companies: software labor. Almost every Fortune 500 company is now a software company in practice. Banks maintain trading systems and compliance platforms. Retailers operate logistics software and personalization engines. Manufacturers run connected factories and digital twins. Pharmaceutical companies depend on data pipelines and research systems. Insurers, airlines, telecoms, energy providers, and governments all maintain large internal codebases. A tool that can accelerate software work has budget relevance far beyond the technology sector.

The API business remains critical, but its strategic role differs from Codex. APIs allow developers to build custom AI products on OpenAI models. This can generate enormous usage-based revenue, especially when applications scale. Yet API customers are often more capable of switching models or routing workloads across providers. Codex, by contrast, can create workflow-level dependency. Once an enterprise has indexed repositories, configured permissions, integrated with CI/CD, trained teams, and built internal processes around AI coding agents, switching becomes harder.

| Metric | ChatGPT Consumer | ChatGPT Enterprise | Codex | API |

|---|---|---|---|---|

| Primary Value Proposition | Personal productivity and general intelligence access | Secure workplace AI assistant | Software engineering and workflow execution | AI infrastructure for applications |

| Typical Contract Size | Low per-user monthly subscription | Medium to high enterprise seat contract | High enterprise contract plus usage expansion | Variable usage-based spend |

| Switching Cost | Low to moderate | Moderate | High when integrated into repositories and workflows | Moderate, depending on application architecture |

| ROI Measurement | Difficult at individual level | Moderate, often survey-based or productivity-estimated | Strong, based on engineering output and cycle time | Strong if tied to application revenue or cost reduction |

| Competitive Moat | Brand, user habit, model quality | Security, governance, enterprise adoption | Workflow integration, agent reliability, developer ecosystem | Model performance, price, latency, ecosystem tools |

The revenue implication is straightforward: OpenAI’s future valuation multiple will likely depend more on enterprise platform revenue than on chatbot subscriptions. Consumer revenue proves demand. Codex revenue proves operational necessity. Investors typically reward the latter more generously because it indicates durable business integration, account expansion, and a path toward becoming core infrastructure.

Competitive Pressure: Anthropic, Google, GitHub, and the Coding-Agent Arms Race

OpenAI’s Codex push is also a defensive necessity. The coding-agent market has become one of the most strategically contested areas in AI because it sits at the intersection of developers, enterprise budgets, cloud platforms, and software supply chains. Anthropic, Google, Microsoft GitHub, and a long list of AI-native startups are all trying to own the developer workflow.

Anthropic’s challenge is particularly serious because Claude has built a strong reputation among developers for reasoning, code understanding, long-context performance, and cautious instruction following. Anthropic’s enterprise agent direction, including coworker-style systems designed to collaborate on tasks rather than merely answer prompts, directly pressures OpenAI’s attempt to define agentic work. If a company already trusts Claude for code review, document reasoning, and internal analysis, Anthropic can credibly compete for the same enterprise automation budget that OpenAI wants Codex to capture.

Google’s Gemini Code Assist benefits from Google’s ownership of developer infrastructure, cloud relationships, and enterprise productivity distribution. Google can bundle AI coding features into Google Cloud, Android development, Workspace-adjacent workflows, and cloud migration programs. For companies already committed to Google Cloud, Gemini Code Assist can be positioned not as a standalone tool but as part of a larger cloud modernization package. That bundling pressure forces OpenAI to justify Codex on performance, flexibility, and cross-platform neutrality.

GitHub Copilot remains one of the most important competitors because it is already embedded where developers work. Microsoft’s ownership of GitHub, its enterprise relationships, and its ability to integrate Copilot across Visual Studio Code, Azure DevOps, GitHub Actions, Microsoft 365, and Azure gives it a formidable distribution advantage. Copilot also has the benefit of being perceived as a developer-native tool rather than a chatbot extended into coding.

| Competitor | Core Advantage | Threat to Codex | OpenAI Counterposition |

|---|---|---|---|

| Anthropic Cowork-style Agents | Strong reasoning reputation, enterprise trust, long-context strengths | Can win teams that prioritize safety, reliability, and thoughtful code reasoning | Codex can emphasize execution, tool integration, and ChatGPT distribution |

| Google Gemini Code Assist | Cloud bundling, enterprise accounts, Google developer ecosystem | Can be packaged into cloud transformation and Workspace deals | OpenAI can remain cloud-flexible and model-focused across heterogeneous stacks |

| GitHub Copilot | Deep IDE, repository, and pull request integration | Owns developer workflow and has Microsoft enterprise distribution | Codex can compete by moving beyond suggestions into autonomous task execution |

| AI-native Coding Startups | Fast iteration, specialized workflows, developer enthusiasm | Can define new interfaces before incumbents respond | OpenAI can leverage frontier models, capital, brand, and enterprise support |

The competitive battlefield is not simply autocomplete. Autocomplete is now table stakes. The market is moving toward repository-level reasoning, autonomous issue resolution, multi-file refactoring, test generation, release management, security remediation, and infrastructure-as-code automation. The winner will not be the tool that writes the best isolated function, but the platform that safely completes the most valuable engineering work inside real organizations.

That is why OpenAI cannot rely on ChatGPT’s popularity to dominate enterprise AI. Developers are pragmatic. They will adopt the tools that work inside their editors, terminals, repositories, issue trackers, and deployment pipelines. If Codex is not deeply integrated into those environments, it risks becoming a powerful demo rather than a daily system of record. The company’s push into Codex CLI, Codex Sites, Plugins, and workflow integrations should be understood as an answer to this distribution problem.

OpenAI’s Path to IPO: What the S-1 Filing Means for ChatGPT, Codex, and Enterprise Customers

The Enterprise Pivot: Why Fortune 500 Companies Are Paying for Codex Over ChatGPT

Fortune 500 companies are not paying premium prices for Codex because they are impressed by code generation demos. They are paying because software delivery is a bottleneck across nearly every strategic initiative. Digital transformation, cloud migration, cybersecurity remediation, ERP modernization, data platform consolidation, customer experience upgrades, and AI adoption itself all depend on engineering capacity. Most large enterprises have more software work than their teams can complete.

Codex attacks this bottleneck directly. A bank can use it to modernize legacy services, generate tests for critical systems, and accelerate regulatory reporting changes. A retailer can use it to update internal tools, maintain integrations, and improve analytics pipelines. A healthcare company can use it to support compliance-aware engineering workflows. A manufacturer can use it to maintain industrial software, automate documentation, and accelerate internal application development. These are not novelty use cases; they are persistent operational needs.

Large companies also like Codex because it can be governed through familiar software development controls. Unlike many knowledge-work AI deployments, software agents can operate behind review gates. They can create branches rather than directly modifying production. They can be restricted to specific repositories. They can run in sandboxes. Their outputs can be tested. Their work can be reviewed by humans before merging. This makes Codex easier to operationalize than agents that act directly in ambiguous business systems without strong validation.

Another factor is the scarcity and cost of senior engineering talent. Enterprises do not expect Codex to replace their best engineers wholesale. Instead, they want it to amplify senior engineers and reduce the time they spend on repetitive work. If Codex can handle boilerplate, test scaffolding, dependency updates, documentation, codebase exploration, migration drafts, and routine fixes, human developers can focus on architecture, product decisions, security judgment, and complex systems design.

Procurement teams also prefer investments that can be tied to existing budget categories. Codex can be justified as developer productivity software, automation infrastructure, application modernization tooling, or AI transformation spend. ChatGPT Enterprise is often funded through digital workplace or productivity budgets, which can be more diffuse. Codex can tap into engineering budgets that are already large and tied to business-critical outcomes.

The internal champion is different as well. ChatGPT Enterprise may be championed by a chief digital officer, CIO, HR leader, operations executive, or innovation team. Codex is often championed by CTOs, heads of engineering, platform leaders, DevOps directors, and security engineering teams. These buyers understand the cost of engineering bottlenecks and can articulate value in operational terms. They also tend to influence long-term technical architecture decisions.

Fortune 500 adoption is ultimately about trust. Codex must prove that it can respect data boundaries, handle proprietary code safely, avoid leaking secrets, provide audit logs, and integrate with enterprise identity systems. OpenAI’s ability to win these customers depends as much on enterprise-grade controls as on model benchmarks. The larger the customer, the more the buying decision shifts from “How smart is the model?” to “Can we safely operationalize this across thousands of developers?”

Developer Ecosystem: Codex Sites, Plugins, CLI, and Platform Lock-In

OpenAI’s Codex strategy becomes more powerful when viewed as an ecosystem rather than a single assistant. Codex Sites, Plugins, CLI tooling, repository integrations, and developer workflows create a platform surface that can pull developers deeper into OpenAI’s environment. The goal is not merely to help a developer write code; it is to become the layer through which software work is delegated, tracked, reviewed, and improved.

Codex CLI is especially important because the terminal remains one of the most trusted environments for developers. A chat interface is useful, but many engineering tasks happen through command-line tools, local environments, build scripts, package managers, cloud CLIs, and deployment utilities. By placing Codex in the terminal, OpenAI moves closer to the actual execution layer of software development. This reduces context switching and allows agents to interact with the same tools developers already use.

Codex Plugins expand the platform by allowing third-party systems to connect into agent workflows. In an enterprise setting, plugins can connect Codex to issue trackers, documentation systems, observability platforms, security scanners, CI/CD pipelines, package registries, cloud environments, and internal developer portals. Each integration increases usefulness and switching cost. Once an organization has built custom Codex plugins around internal workflows, replacing Codex becomes more expensive.

Codex Sites represent another layer of lock-in: persistent, shareable workspaces where agents, humans, documentation, code artifacts, and task histories can coexist. If OpenAI can make Codex Sites the place where engineering teams manage AI-assisted projects, it gains a collaboration surface beyond the IDE. That matters because the future of AI software development is not just individual coding acceleration; it is team-level coordination between humans and agents.

The platform lock-in mechanism is subtle but powerful. At first, a developer uses Codex to solve a small issue. Then a team connects it to a repository. Then they add CI/CD access. Then they configure policy rules. Then they integrate security scanning. Then managers begin tracking AI-assisted throughput. Then internal documentation references Codex workflows. At that point, Codex is no longer a tool that can be casually swapped out. It has become part of the organization’s engineering operating model.

This is the same pattern that made developer platforms historically sticky. GitHub became more than Git hosting because it absorbed issues, pull requests, Actions, security scanning, packages, and collaboration. AWS became more than compute because it absorbed databases, identity, messaging, monitoring, and deployment. OpenAI’s Codex ecosystem is attempting a similar expansion around AI-executed software work.

The risk is that developers resist closed ecosystems. Developer trust is earned through reliability, transparency, portability, and respect for existing workflows. If Codex feels like a black box, or if it attempts to force developers into proprietary patterns too aggressively, it will face pushback. The most successful version of Codex will likely be deeply integrated but not suffocating: powerful inside OpenAI’s ecosystem, yet flexible enough to work across GitHub, GitLab, Bitbucket, Azure DevOps, JetBrains, VS Code, local terminals, and multiple clouds.

Will ChatGPT Become a Codex Frontend for Consumers?

For consumers, the rise of Codex raises a provocative question: will ChatGPT become a Codex frontend? The answer is yes in some contexts, but not in the narrow sense that ChatGPT will become only a coding interface. Rather, ChatGPT is likely to become a general-purpose agent frontend, with Codex serving as one of the most advanced and commercially important agent modules beneath it.

Most consumers will not think in terms of Codex. They will ask ChatGPT to build a website, create a spreadsheet automation, fix a script, connect an app, analyze a dataset, generate a workflow, or prototype a product idea. Behind the scenes, Codex-like capabilities may create files, run code, deploy a small application, configure integrations, or debug errors. The user experience remains conversational, but the underlying system becomes agentic.

This creates a major opportunity for OpenAI in consumer software creation. Millions of users want to build digital tools but do not identify as developers. If ChatGPT can turn natural language requests into working applications, automations, websites, and data tools, it expands the market for software creation. Codex becomes the engine that turns intent into functioning artifacts.

However, this also changes consumer expectations. Users will no longer be satisfied with answers that explain how to do something. They will expect ChatGPT to complete the task. A user who asks for a personal budget tracker may expect a working app. A small business owner who asks for an inventory tool may expect a deployable system. A creator who asks for a landing page may expect hosting, analytics, and revisions. The standard of usefulness rises dramatically.

There are limits. Consumer-facing agentic software creation must handle security, privacy, payments, data storage, hosting, and maintenance. Building a prototype is easier than maintaining production software. OpenAI must decide how much of the software lifecycle it wants ChatGPT to own for non-technical users. If the company pushes too far without strong guardrails, it risks creating fragile applications that users do not know how to maintain.

The more likely path is tiered capability. Free and consumer users receive guided creation and limited execution. Professional users receive deeper workflows, hosting options, and integrations. Enterprise users receive governed Codex deployments with private repositories, compliance controls, and administrative oversight. In all tiers, ChatGPT remains the interface, but Codex-style execution becomes increasingly central to the value proposition.

Timeline: From Chatbot Breakthrough to Agent Platform

OpenAI’s evolution can be understood as a progression from model access to conversation, then from conversation to tools, and finally from tools to agents. Codex is not an isolated detour; it is part of the company’s broader movement toward AI systems that can perform work across digital environments.

| Period | Product Milestone | Strategic Meaning |

|---|---|---|

| 2021 | Early Codex and code-generation capabilities emerge as a major demonstration of transformer utility | Software becomes one of the first domains where generative AI shows clear productivity potential |

| 2022 | ChatGPT launches and becomes the public face of generative AI | Conversation becomes the dominant interface for mainstream AI adoption |

| 2023 | ChatGPT Plus, plugins, API expansion, and enterprise interest accelerate | OpenAI begins converting consumer demand into a platform and enterprise opportunity |

| 2024 | Multimodal models, stronger tool use, enterprise controls, and coding improvements mature | The market starts shifting from chat responses to AI-assisted workflows |

| 2025 | Agent frameworks, deeper developer tools, and Codex-style task execution become central to enterprise pilots | Enterprises begin paying for measurable automation rather than broad experimentation |

| 2026 | Codex capabilities increasingly merge into ChatGPT and enterprise agent deployments | OpenAI’s narrative shifts from chatbot company to enterprise AI platform for delegated digital work |

This timeline shows why the “ChatGPT versus Codex” framing can be misleading. ChatGPT created the market. Codex monetizes the work. The strategic future likely belongs to the combination: a familiar conversational interface connected to specialized agents that perform tasks in software, data, operations, and enterprise systems.

Expert Analysis: The IPO Narrative Is Changing

If OpenAI eventually pursues a public listing, the company will need to explain itself in terms that public-market investors understand. A pure chatbot narrative would raise difficult questions. How durable are consumer subscriptions? How expensive is inference? How vulnerable is the product to bundling by Apple, Google, Microsoft, Meta, or device manufacturers? How much pricing power exists when high-quality AI assistants become widely available?

A Codex-centered narrative is stronger. It positions OpenAI as an enterprise AI platform capable of automating high-value digital work. That story connects to large budgets, recurring contracts, workflow lock-in, developer ecosystems, and measurable productivity gains. It also allows OpenAI to argue that its models are not just content generators but labor engines embedded in the software economy.

Public-market investors tend to reward companies that become systems of record or systems of action. ChatGPT is a system of interaction. Codex has the potential to become a system of action. It can create, modify, test, and manage software artifacts. If extended carefully, the same agentic pattern can apply to data operations, financial analysis, customer support, legal workflows, and internal business processes. Codex is the template for that larger ambition.

The challenge is that enterprise platform stories come with enterprise scrutiny. OpenAI will need to demonstrate retention, expansion, gross margin discipline, security posture, compliance maturity, and reliable customer outcomes. It will need to show that agentic AI can scale safely without creating unacceptable operational risk. It will also need to manage compute costs, which remain one of the biggest constraints on profitability in frontier AI.

Another IPO consideration is concentration risk. If Codex revenue depends heavily on large enterprise contracts, OpenAI will need to prove that adoption is broad across sectors and not limited to a few marquee customers. If API revenue is exposed to price competition, OpenAI will need to show that platform services and agent products create defensibility. If consumer ChatGPT growth slows, OpenAI will need to show that ChatGPT remains a distribution advantage rather than a maturing subscription product.

In this context, the merger of Codex and ChatGPT becomes central to the investment thesis. ChatGPT provides top-of-funnel distribution and user familiarity. Codex provides enterprise monetization and workflow depth. The API provides developer reach and application infrastructure. Together, they form a more credible platform narrative than any one product alone.

Strategic Risks: Why Codex Could Still Fall Short

The bullish case for Codex is compelling, but it is not guaranteed. The first major risk is reliability. Software engineering agents must handle complex codebases, hidden dependencies, ambiguous requirements, and organization-specific conventions. Passing a benchmark is not the same as safely modifying a production system with years of technical debt. If Codex produces too many flawed pull requests, developers may treat it as noise rather than leverage.

The second risk is security. Coding agents need access to sensitive repositories, internal documentation, build systems, credentials, and deployment environments. Even with strong controls, this creates new attack surfaces. Enterprises will demand granular permissions, secret redaction, audit logs, data residency options, policy enforcement, and clear liability boundaries. A major security incident involving agentic code modification could slow adoption across the entire market.

The third risk is developer culture. Developers are not passive software buyers. They have strong opinions about tooling, workflow, and trust. If Codex is perceived as management surveillance, low-quality automation, or an attempt to deskill engineering teams, adoption could face internal resistance. OpenAI must position Codex as an amplifier of engineering judgment, not a replacement for it.

The fourth risk is competition from embedded incumbents. GitHub, Microsoft, Google, JetBrains, Atlassian, GitLab, and cloud providers all have natural distribution points in developer workflows. OpenAI’s model advantage may not be enough if competitors own the surfaces where developers spend their time. This is why OpenAI’s integration strategy is as important as its model strategy.

The fifth risk is economics. Agentic workflows can be compute-intensive because they involve planning, tool calls, code analysis, test execution, retries, and long context. If pricing does not cover inference and infrastructure costs, rapid adoption could pressure margins. OpenAI must balance capability, latency, reliability, and cost in a way that supports enterprise-scale profitability.

Despite these risks, Codex remains strategically essential because the alternative is worse. If OpenAI stayed primarily focused on conversational AI while competitors captured developer workflows and enterprise agents, it would risk becoming the most famous interface in a market where the deepest revenue moved elsewhere. Codex is OpenAI’s attempt to own the execution layer before others define it.

Access 40,000+ AI Prompts for ChatGPT, Claude & Codex — Free!

Subscribe to get instant access to our complete Notion Prompt Library — the largest curated collection of prompts for ChatGPT, Claude, OpenAI Codex, and other leading AI models. Optimized for real-world workflows across coding, research, content creation, and business.

Conclusion: ChatGPT Is the Door, Codex Is the Business

ChatGPT is not disappearing, and it is not becoming irrelevant. It remains one of the most important technology products of the last decade and the interface that made AI mainstream. But it is no longer sufficient to describe OpenAI’s strategic future. The company’s next phase is being shaped by agents, developer platforms, enterprise workflows, and systems that do work rather than merely discuss it.

Codex represents this transition more clearly than any other OpenAI product. It converts model intelligence into operational output. It gives enterprises a measurable productivity story. It creates opportunities for platform lock-in through repositories, terminals, plugins, sites, and workflow integrations. It gives OpenAI a stronger IPO narrative than consumer chatbot subscriptions alone. Most importantly, it points toward the future of AI as delegated digital labor.

The evidence suggests that OpenAI’s highest-value growth is increasingly tied to Codex and agentic enterprise deployments. Consumer ChatGPT remains the brand engine. ChatGPT Enterprise remains the safe enterprise entry point. The API remains the developer infrastructure layer. But Codex is becoming the product that best captures where the money, urgency, and defensibility are moving.

For consumers, this means ChatGPT will increasingly feel less like a chatbot and more like a task environment. For developers, it means coding agents will become standard parts of the software lifecycle. For enterprises, it means AI budgets will shift from experimentation to operational automation. For OpenAI, it means the company’s future will be judged less by how many people chat with its models and more by how much work its agents can reliably complete.

The defining OpenAI product of the public imagination is still ChatGPT. The defining OpenAI product of the enterprise future may be Codex. That is the strategic shift now reshaping the company: from conversation to execution, from chatbot to agent platform, and from AI that answers to AI that acts.